The Yen Carry Trade is a massive global financial mechanism that has historically kept U.S. borrowing costs low but now poses a risk of sudden volatility for American homeowners and investors.

The Yen Carry Trade Explained

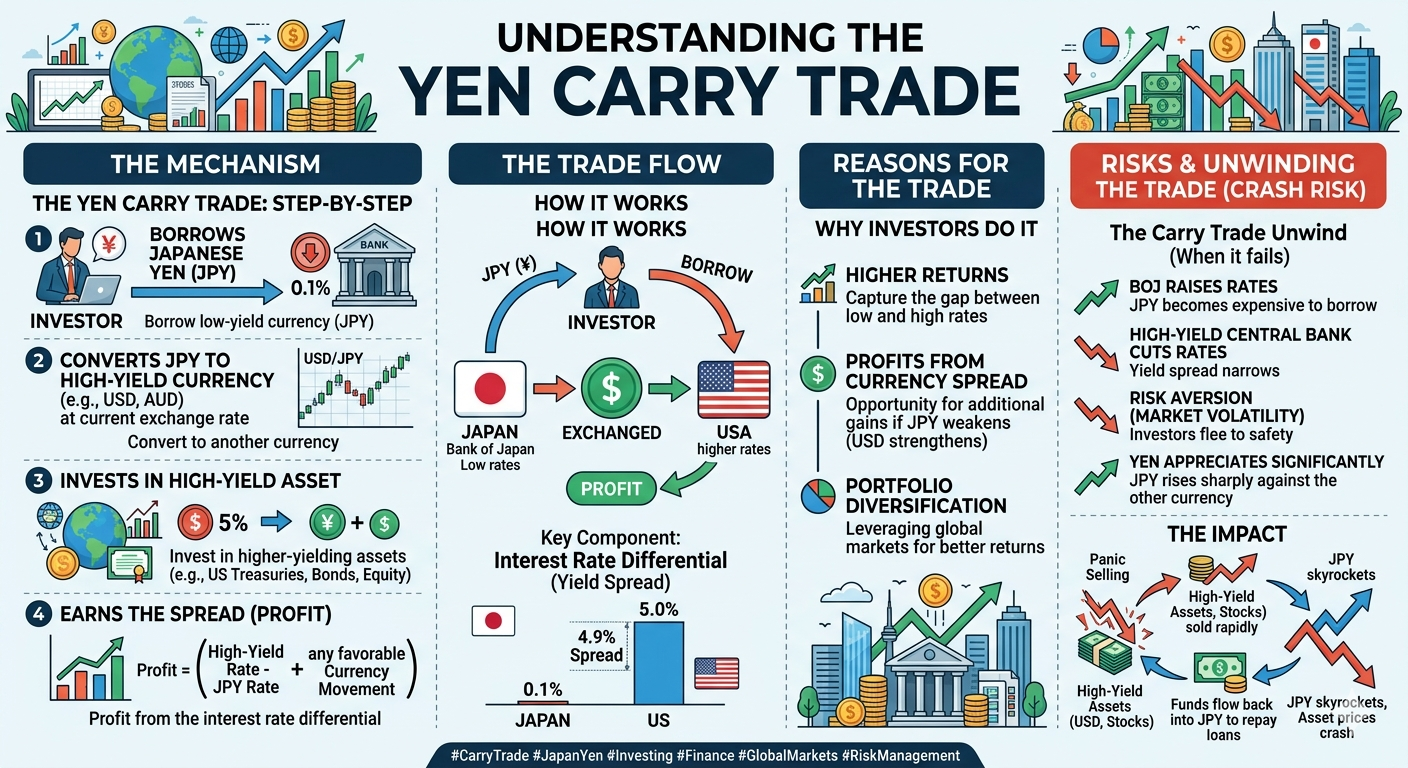

A “carry trade” is an investment strategy where a trader borrows money in a currency with a very low interest rate and reinvests it in assets that offer a higher return.

- The Funding Source: For decades, the Bank of Japan (BoJ) maintained near-zero or negative interest rates to combat deflation, making the Japanese yen the world’s cheapest currency to borrow.

- The Investment: Traders take these cheap yen, convert them into U.S. dollars, and buy higher-yielding assets like U.S. Treasury bonds, tech stocks, or mortgage-backed securities (MBS).

- The Profit: The investor profits from the “spread”—the difference between the 0% cost of borrowing yen and the 4%–5% yield on U.S. assets.

Impact on the US Housing Market

The yen carry trade acts as a hidden support pillar for U.S. real estate. When this trade is active, it creates a steady stream of “cheap” Japanese-funded capital flowing into the U.S..

- Lower Mortgage Rates: A significant portion of carry trade capital is invested in U.S. Treasury bonds and MBS. This high demand pushes bond prices up and yields down. Since mortgage rates track the 10-year Treasury yield, this “subsidizes” cheaper home loans for Americans.

- The “Unwind” Risk: If Japan raises interest rates (as seen in late 2024 and early 2025), the trade becomes less profitable. Investors are forced to sell their U.S. bonds and MBS to pay back their yen loans. This mass selling causes:

- Bond yields to spike, which can immediately drive up mortgage rates.

- Tightened credit, making it harder for buyers to qualify for loans as global liquidity dries up.

Pros and Cons of the Yen Carry Trade

How the US Can Defend Its Housing Market

Preventing the impact of the yen carry trade is difficult because it involves the sovereign policy of another nation, but the U.S. can “defend” its market through several mechanisms:

- Treasury Intervention: The U.S. Treasury can coordinate with Japan to manage currency fluctuations, preventing the yen from strengthening too quickly and triggering a “panic” unwind.

- Federal Reserve Liquidity: If a carry trade unwind causes a sudden spike in mortgage rates, the Federal Reserve can step in as a “buyer of last resort” for U.S. Treasuries and MBS to stabilize yields.

- Macro-Prudential Regulations: Regulators can impose stricter leverage limits on banks and hedge funds participating in carry trades, ensuring that a single “bad day” in the yen doesn’t lead to a systemic collapse in U.S. credit markets.

- Fiscal Stability: Reducing the U.S. trade deficit and reliance on foreign debt can make the U.S. housing market less sensitive to whether or not Japanese investors decide to buy our bonds.

Common Misconceptions

While the yen carry trade influences global liquidity, U.S. mortgage rates are primarily driven by a combination of domestic economic indicators, government policy, and market dynamics.

1. Inflation and Treasury Yields

- 10-Year Treasury Yield: This is the most critical benchmark for 30-year fixed mortgages.

- As Treasury yields rise due to investor expectations of growth or inflation, mortgage rates typically follow to remain competitive.

- Inflation Trends: Inflation erodes the purchasing power of future interest payments.

- Lenders demand higher rates when inflation is high to protect their real profit margins.

2. Federal Reserve Policy

- Federal Funds Rate: The Fed does not set mortgage rates directly but influences the “cost of money” for banks.

- When the Fed raises its benchmark rate to cool the economy, it indirectly pushes up long-term mortgage rates.

- Monetary Messaging: Market expectations of future Fed cuts or hikes often move mortgage rates well before the Fed officially acts.

3. Secondary Market Dynamics

- Mortgage-Backed Securities (MBS): Most mortgages are bundled into bonds and sold to investors.

- If investor demand for these bonds drops (due to higher risk or better returns elsewhere), yields and mortgage rates must rise to attract buyers.

- The “Spread”: This is the difference between the 10-year Treasury yield and the 30-year mortgage rate.

- Economic uncertainty or high volatility can cause this spread to widen, keeping mortgage rates high even if Treasury yields are falling.

4. Broader Economic Health

- Gross Domestic Product (GDP): Strong economic growth typically leads to higher demand for credit, which can push interest rates upward.

- Labor Market: High employment and rising wages can fuel inflation, leading to higher rates. Conversely, a weak job market often signals a slowing economy, which may pull rates down.

5. Housing Market Supply and Demand

- Lender Competition: When demand for new mortgages is low, lenders may lower their profit margins (reducing the spread) to attract more borrowers.

- Inventory Levels: Limited housing supply can sustain high prices, which may keep the total demand for mortgage credit and thus rate elevated.

6. Geopolitical and Fiscal Factors

- “Flight to Safety”: During global crises, international investors often rush to buy U.S. Treasuries, which drives yields down and can temporarily lower mortgage rates.

- Fiscal Deficits: Large government deficits require the U.S. to issue more debt, which can push interest rates higher to attract enough buyers for those bonds.